Electric Vehicle Charging Station Market – (By Connector Protocol – CHAdeMO, CCS, and Others; By Charger Type – Slow Charging and Fast Charging; By Charging Method – AC Charging and DC Charging; By Charging Station Type – Public, Semi-Public, and Private; By Application – Commercial and Residential); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2050

- Last Updated: 10-Feb-2026 | | Report ID: AA0421078

Market Snapshot

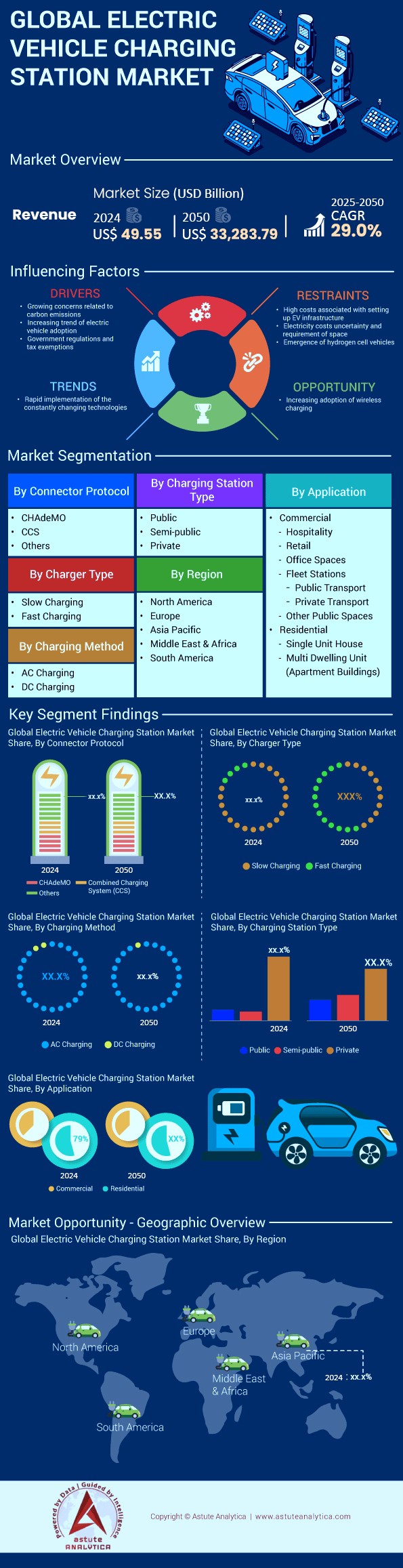

Electric vehicle charging station market is projected to increase from US$ 63.92 billion in 2025 to US$ 33,283.79 billion by the end of 2050 at a robust CAGR of 29.0% during the forecast period 2026–2050.

- By Charger Types: Slow Charging (<=22kW) control over 81.80% market share

- By Charging Methods: DC Charging control over 95.30% market share

- By Applications: Residential application of the charging station take up more than 56% market share of the electric vehicle charging station market.

- By Charging Station Types: Private charging station capture over 88.20% market share

- Asia Pacific, particularly China, has solidified its position as the global leader in electric vehicle charging station market by controlling more than 80.65% market share.

The global electric vehicle (EV) charging station market is currently undergoing a radical metamorphosis. We are shifting from an era of "Range Anxiety" to one of "charging anxiety," and finally, to "grid integration." As of early 2026, the market is no longer defined merely by the number of plugs installed, but by uptime reliability, utilization rates, and energy management sophistication.

While the broader electric vehicle market has seen fluctuations in demand, the infrastructure sector remains an absolute imperative, the vehicles cannot exist without the plugs. The market is pivoting from a hardware-centric model to a Software-Defined Energy Services model.

Strategic Scope of the electric vehicle charging station market:

- Hardware (EVSE): From 3kW residential units to 1MW+ commercial trucking chargers.

- Software (CMS): Charge Management Systems, OCPP protocols, and payment gateways.

- Services: EPC (Engineering, Procurement, Construction) and O&M (Operations & Maintenance).

The most significant trend for the electric vehicle charging station market during 2026-2050 is the consolidation of standards (NACS/J3400 dominance) and the financialization of charging assets, where utilization rates and electricity arbitrage become the primary revenue drivers over hardware margins.

To Get more Insights, Request A Free Sample

Supply Chain, Component Costs, and Manufacturing

EV chargers are sophisticated computers. They rely heavily on power electronics. The shift from Silicon (Si) to Silicon Carbide (SiC) MOSFETs in charger power modules is increasing efficiency by reducing heat loss, but SiC supply chains are tight.

Localization (BABA/Made in America):

To qualify for US federal NEVI funds, chargers must be manufactured in the US with 55% domestic component cost. This has forced global players (ABB, Tritium, Wallbox) in the electric vehicle charging station market to open factories in Tennessee, South Carolina, and Texas.

- Raw Materials: The cost of copper (for cables) and steel (for enclosures) impacts the final price. A DC Fast Charger costs between $25,000 (50kW) to $150,000 (350kW) installed. Soft costs (permitting, trenching, grid upgrades) often exceed the hardware cost.

Competitive Landscape & Market Share Concentration

The electric vehicle charging station market is fragmented but consolidating rapidly.

- The Hardware Giants: ABB E-mobility and Tritium (liquidated/acquired assets) traditionally dominated, but Asian manufacturers (SK Signet) are gaining ground in the US.

- The Energy Pivots: Oil and Gas supermajors (Shell Recharge, BP Pulse, TotalEnergies) are aggressively acquiring CPOs. They have the real estate (gas stations) and the capital to weather the initial low-utilization years.

- The Pure Plays: Companies like ChargePoint (Asset-light model) and EVgo (Asset-heavy model) face pressure to reach profitability. ChargePoint controls the AC market share in North America but faces fierce competition in DCFC.

- The Automakers: IONITY (BMW, Ford, Hyundai, Mercedes, VW) in Europe and the Ionna JV in North America represent OEMs taking destiny into their own hands to ensure their customers have a place to charge.

Analysis of Technological Segmentation: The War of Protocols & Power in the Electric Vehicle Charging Station Market

The hardware landscape is being redefined by two factors: The consolidation of connector standards and the thermal management of high-power cables.

The Connector Consolidation (NACS/J3400 vs. CCS):

The "Plug War" in North America has effectively ended with the victory of the North American Charging Standard (NACS/SAE J3400). Following Ford and GM’s adoption, the market is now in a transitional phase where "Magic Docks" (adapters) are a temporary bridge. In Europe, CCS2 remains the mandated standard, creating a bifurcated global manufacturing supply chain. In China, the transition is from GB/T to ChaoJi, a standard capable of ultra-high power delivery co-developed with Japan.

Power Output Dynamics (The 350kW Race):

Third-generation EVs (800V architectures like the Hyundai Ioniq 5/6, Porsche Taycan) demand 350kW charging speeds. The electric vehicle charging station market is phasing out 50kW DC chargers (once standard) in favor of 150kW modular units that can share power. If one car charges, it gets 150kW; if two charge, they split 75kW/75kW. This "Dynamic Power Sharing" is critical for reducing grid connection costs.

Liquid Cooled Cables:

To achieve speeds above 300 Amps, standard copper cables become too heavy for consumers to lift. The electric vehicle charging station market is seeing a 100% attach rate of liquid-cooled cable systems for Ultra-Fast Charging (UFC) stations, significantly increasing the Bill of Materials (BOM) cost but enabling sub-20-minute charge times.

The Rise of Megawatt Charging Systems (MCS) & Heavy-Duty Infrastructure

While passenger EVs grab headlines, the commercial transport sector offers the highest density of energy consumption and predictable revenue streams.

The MCS Standard: The Megawatt Charging System (MCS) is designed for Class 8 trucks and heavy-duty logistics. Unlike passenger car chargers (max ~350-500kW), MCS targets 3.75 MW (3,000 Amps at 1,250 Volts). This allows a long-haul truck to replenish its battery during the legally mandated 45-minute driver break.

Depot vs. En-Route:

- Depot Charging (Overnight): Low power (50-100kW), long dwell time. This is currently 90% of the electric vehicle charging station market.

- En-Route (Public): High power (MCS), short dwell time. This segment is nascent but critical for the "Middle Mile" logistics electrification.

- ROI Implication: For fleet operators, the TCO (Total Cost of Ownership) parity is reached not just by cheaper fuel, but by predictable charging costs. Hence, we are seeing the rise of "Charging-as-a-Service" (CaaS) for fleets, where infrastructure costs are bundled into a per-mile operational expense.

Impact of Smart Charging, V2G, and Grid Integration on Electric Vehicle Charging Station Market

The grid is the ultimate bottleneck for the electric vehicle charging station market. Upgrading transformers is slow and expensive. Smart charging is the software patch for a hardware problem.

- V1G (Smart Charging): Unidirectional control. The charger lowers output when the grid is stressed. This is becoming mandatory in jurisdictions like the UK (Smart Charge Points Regulations).

- V2G (Vehicle-to-Grid): Bi-directional power. The EV battery acts as a distributed energy resource (DER).

- Status: Moving from pilot to commercial. Standards like ISO 15118-20 enable this.

- Value Prop: An EV owner can earn money by selling excess energy back to the grid during peak pricing hours (arbitrage).

- Plug & Charge (ISO 15118): This technology eliminates apps and credit cards. The car identifies itself to the charger via encrypted certificates. This "Tesla-like" seamless experience is finally rolling out across the CCS/NACS ecosystem, reducing friction and increasing user satisfaction.

The Battery Swapping Niche: Dead or Alive?

Western media often dismisses battery swapping, but the data suggests a bifurcated reality in the electric vehicle charging station market.

- Passenger Vehicles: In the US and Europe, swapping is niche due to the structural battery packs (cell-to-chassis) used by Tesla and BYD, which make batteries non-removable. However, NIO continues to expand its Power Swap Stations in Europe, betting on "Battery as a Service" (BaaS) to lower the upfront car cost.

- Two/Three Wheelers: In India and Southeast Asia (ASEAN), battery swapping is the dominant form of electrification (e.g., Gogoro). The batteries are light, the vehicles are cheap, and downtime is unacceptable for delivery drivers.

- Heavy Trucking: There is a resurgence of interest in automated battery swapping for trucks (e.g., Ample), as swapping a massive truck battery takes 5 minutes versus the 45+ minutes required for megawatt charging.

Business Model Evolution: CPOs, MSPs, and MaaS

The electric vehicle charging station market is moving away from a simple "hardware sales" model.

CPO vs. MSP:

- Charge Point Operator (CPO): Owns and maintains the hardware (e.g., Electrify America, Ionity). Their asset is the plug.

- Mobility Service Provider (MSP): Owns the customer relationship and the app (e.g., Shell Recharge, BMW Charging). Their asset is the data.

- Roaming (eRoaming): Hubs like Hubject allow an MSP user to charge at a CPO station. This interoperability is becoming standard, similar to cellular roaming.

Revenue Stacking: Successful players in 2026 are "revenue stacking." They combine:

- Charging fees (per kWh or per minute).

- Grid Services (Demand Response participation).

- Digital Out-of-Home (DOOH) advertising on 55-inch charger screens.

- Carbon Credit trading (LCFS credits in California/British Columbia).

Segmental Analysis of the Electric Vehicle Charging Station Market

By Charger Types: Slow Charging (≤22kW) Dominating the Market

Market Share: 81.80% (Dominant in Installed Volume)

The "Base Load" of Infrastructure segment, primarily consisting of AC Level 1 and Level 2 chargers, forms the capillary network of the EV ecosystem. The 81.80% dominance stems from the technical reality that the average personal vehicle sits idle for over 90% of the day, making low-power (<22kW) charging the most logical solution for battery replenishment without degrading battery health.

- Grid Synergy: Unlike high-power alternatives, ≤22kW chargers in the electric vehicle charging station market are less likely to trigger demand charges or require massive grid upgrades (transformers) at the local distribution level. This segment is currently the testbed for Smart Charging (V1G) and Vehicle-to-Grid (V2G) technologies, where slow charging speeds allow for dynamic load balancing during peak grid hours.

- Cost vs. Utility: The widespread adoption is driven by the low CAPEX (Capital Expenditure). A typical 7kW-22kW AC wallbox costs a fraction of a DC fast charger, allowing for massive proliferation in diverse settings (homes, offices, retail parking) where "dwell time" exceeds 2-4 hours.

By Charging Methods: DC Charging Emerged as the Most Popular Revenue Generator

Market Share: 95.30% (Dominant in Market Value/Commercial Revenue)

While lower in volume count compared to AC chargers, DC charging controls ~95.3% of the electric vehicle charging station market’s financial value and strategic focus. This disparity exists because a single ultra-fast DC charging station (150kW–350kW) represents an investment of $50,000 to $150,000+ compared to <$1,000 for an AC unit.

- The "Corridor" Enabler: The DC charging is the sole solution for Range Anxiety on highways. The dominance here reflects the intense build-out of "Electric Highways" and public corridor networks (e.g., NEVI program in the US, TEN-T in Europe). It is technically distinct as it bypasses the vehicle’s On-Board Charger (OBC), delivering power directly to the battery management system (BMS).

- Technological Shift: The segment in the global electric vehicle charging station market is moving aggressively toward Liquid-Cooled Cables and 800V architectures (to match newer EVs like the Porsche Taycan or Hyundai Ioniq 5). The high market share also captures the burgeoning e-Fleet and e-Bus sectors, where high-power DC charging (overhead pantographs or heavy-duty plugs) is mandatory for operational efficiency.

By Applications: Residential Application to Continue Holding Dominance in Electric Vehicle Charging Station Market

Market Share: >56%

The 56% market share validates the electric vehicle charging station market’s adage that "home is the primary fueling station." This segment is heavily correlated with early EV adopter demographics—homeowners with off-street parking. It is the most sticky segment; once a residential charger is installed, user reliance on public charging drops by over 80%.

- Energy Management Integration: This is no longer just about "plugging in." The granular growth in this segment across the electric vehicle charging station market is driven by the integration of EV chargers with Home Energy Management Systems (HEMS) and Rooftop Solar PV. Modern residential units are increasingly being sold as "solar-ready," allowing users to charge strictly from excess solar generation, effectively achieving zero-emission mobility.

- Shadow Market: A significant portion of this market remains "dumb" or unmanaged charging, but regulatory shifts (like the UK’s Electric Vehicles (Smart Charge Points) Regulations) are forcing a rapid transition to connected, smart-enabled residential units to prevent local brownouts.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Charging Station Types: Private Charging Station Enjoying the Lead in Electric Vehicle Charging Station Market

Market Share: 88.20%

The overwhelming dominance of the private stations (homes, private office depots, fleet yards) indicates that the public charging network is essentially a "top-up" or emergency service rather than the primary fuel source for the majority of EV drivers.

- Fleet Depot Dominance: Beyond residential, this figure captures the massive privatization of charging for commercial logistics (Last-mile delivery vans like Amazon/Rivian or DHL). These logistics giants build private, "behind-the-fence" hubs to ensure 100% uptime and avoid the volatility of public charging pricing.

- Real Estate Value: Private charging is transitioning from a niche amenity to a real estate requirement. In multi-unit dwellings (condos/apartments), the installation of private charging infrastructure is becoming a critical asset for property valuation, despite the "Right to Charge" legal complexities facing tenants in many jurisdictions.

To Understand More About this Research: Request A Free Sample

Regional Analysis of the Electric Vehicle Charging Station Market

Asia-Pacific: China’s Dominance Shape the Market

China is not just a market leader, it is a market outlier. As of January 2026, China accounts for approximately 60-65% of the global public charging stock. The dominance of the country is driven by the "New Infrastructure" initiative and state-owned giants like State Grid Corporation of China and private heavyweights like TELD and Star Charge.

Moreover, due to high-density housing (few private garages), China leads the global electric vehicle charging station market when it comes to public AC slow charging piles. In fact, the country has the only commercially viable battery-swapping ecosystem (NIO).

Japan and South Korea amplify this lead of the Asia Pacific region in the electric vehicle charging station market with precision engineering—Toyota's rapid charger networks support hydrogen-EV hybrids, while Hyundai-Kia's ecosystem prioritizes ultrafast DC stations for fleet efficiency.

India's bustling corridors now feature solar-powered hubs, addressing power density challenges innovatively. Private giants like NIO's battery-swapping stations and State Grid's nationwide backbone eliminate range anxiety, fueling consumer confidence.

This regional supremacy stems from synchronized EV manufacturing booms—BYD and CATL's vertical integration ensures chargers match production velocity. Urban density demands dense networks, unlike sprawling Western grids still grappling with permitting delays.

Europe: The Regulation Laboratory

Europe is the most mature regulatory market in the global electric vehicle charging station market, driven by the Alternative Fuels Infrastructure Regulation (AFIR), which mandates charging pools every 60km along the TEN-T core network.

- The Nordic Model: Norway and the Netherlands serve as the crystal ball for the rest of the world. With EV penetration over 80% in Norway, the challenge has shifted from "range anxiety" to "queue anxiety" and grid congestion.

- Germany: As the automotive heartland, Germany is heavily investing in the Deutschlandnetz (German Network), a government-tendered HPC network to ensure coverage in unprofitable rural areas.

North America: The Sleeping Giant Wakes

The US electric vehicle charging station market has historically lagged due to geographical vastness and inconsistent federal policy.

- NEVI Funding: The National Electric Vehicle Infrastructure (NEVI) Formula Program ($5B) is currently the biggest driver, mandating 97% uptime reliability—a direct response to the poor reliability of legacy networks.

- Tesla’s Supercharger Network: This remains the gold standard. As Tesla opens its network to non-Tesla EVs, it effectively becomes the largest public utility for transport energy in North America, creating a near-monopoly on high-speed reliable charging.

Top 5 Major Company Developments in Electric Vehicle Charging Station Market

- Tata Power (India): Announced plans to deploy 1,200+ public-private EV charging stations across India, leveraging grid integration and franchise models for nationwide coverage.

- Adani TotalEnergies E-Mobility (ATEL, under Adani Total Gas) invested ₹100 crore by May 2025 for 3,400 stations nationwide (2,338 energized), targeting airports and highways, with plans for 2,000 more points.

- Wallbox (USA): Expanded partnership with Codale Electric to upgrade existing stations and build new AC/DC fast chargers across Utah, Idaho, Wyoming, and Nevada.

- State Grid Corporation of China: Announced deployment of 1 million additional public charging piles nationwide by end-2025 under the "New Infrastructure" plan, achieving 20 million total facilities with 98% highway service area coverage and average 46.5kW power per unit.

- Electrify America (US): Announced 500 new Hyper-Fast charging stations across major US highways in 2025, featuring 350kW+ NACS/J3400 ports with dynamic power sharing and 97% uptime guarantees under NEVI compliance.

Top Companies in the Electric Vehicle Charging Station Market

- ABB Ltd.

- Blink Charging Co.

- BP Chargemaster Ltd.

- Broadband TelCom Power, Inc.

- Delta Electronics, Inc.

- Evgo

- Efacec Electric Mobility

- Infineon Technologies

- POD Point

- Shell plc

- Shenzhen Setec Power Co., Ltd.

- AeroVironment Inc.

- BYD Auto

- ChargePoint, Inc.

- Other Prominent Players

Market Segmentation Overview

By Connector Protocol:

- CHAdeMO

- CCS

- Others

By Charger Type:

- Slow Charging

- Fast Charging

By Charging Method:

- AC Charging

- DC Charging

By Charging Station Type:

- Public

- Semi-public

- Private

By Application:

- Commercial

- Hospitality

- Retail

- Office Spaces

- Fleet Stations

- Public Transport

- Private Transport

- Other Public Spaces

- Residential

- Single Unit House

- Multi Dwelling Unit (Apartment Buildings)

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Russia

- Spain

- Poland

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 63.92 Bn |

| Expected Revenue in 2050 | US$ 33,284 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2050 |

| Unit | Value (USD Bn) |

| CAGR | 29.0% |

| Segments covered | By Charger Type, By Connector Protocol, By Charging Method, By Charging Station Type, By Application, By Region |

| Key Companies | ABB Ltd., Blink Charging Co., BP Chargemaster Ltd., Broadband TelCom Power, Inc., Delta Electronics, Inc., Evgo, Efacec Electric Mobility, Infineon Technologies, POD Point, Shell plc, Shenzhen Setec Power Co., Ltd., AeroVironment Inc., BYD Auto, ChargePoint, Inc., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

The market will surge from $63.92 billion in 2025 to $33,283.79 billion by 2050, achieving a robust 29.0% CAGR, fueled by infrastructure mandates and fleet electrification demands.

China's state-backed New Infrastructure initiative and giants like State Grid deploy millions of chargers, matching BYD/CATL's EV boom with dense urban networks and battery swapping.

NACS victory in North America ends the plug war, enabling seamless 350kW charging via adapters; Europe sticks to CCS2, while China's ChaoJi eyes ultra-high power, streamlining manufacturing.

DC fast chargers ($50K-$150K each) power highways and fleets, bypassing onboard limits for sub-20-minute sessions, capturing premium corridor revenue over cheap AC home units.

V1G dynamically cuts peaks; V2G turns EVs into grid batteries via ISO 15118, enabling owners to arbitrage energy sales. UK mandates accelerate this shift from dumb plugs.

Private depots ensure 100% uptime for logistics like Amazon, bundling CaaS into per-mile costs for TCO parity, far outperforming volatile public networks.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |